Author: Jasmin Fraser

Date: 2 December 2024

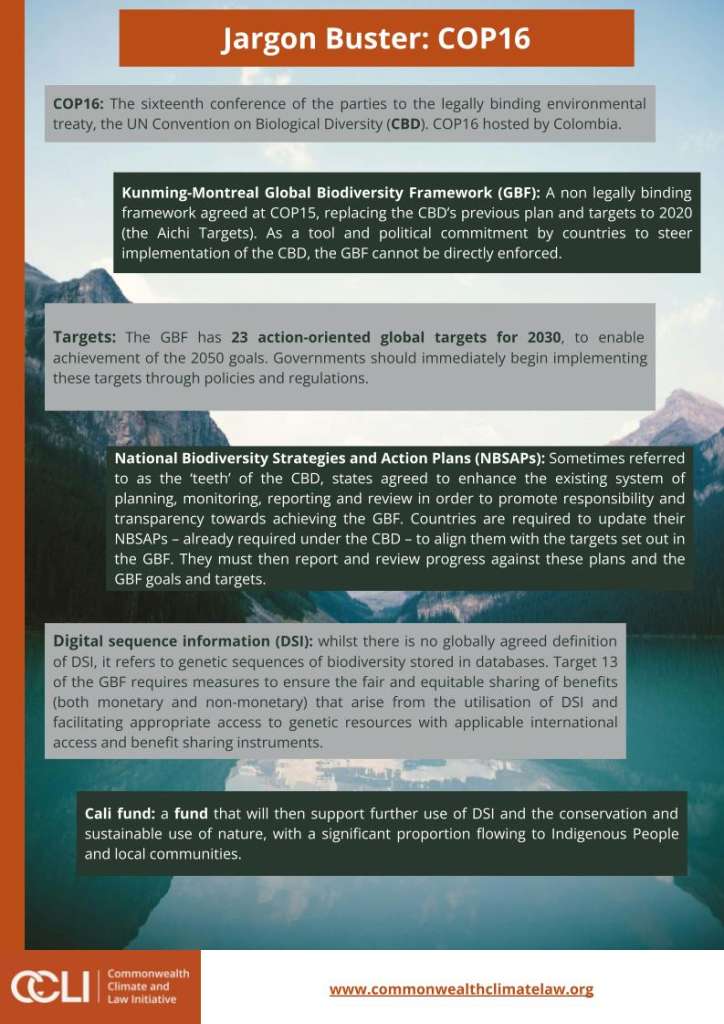

The 16th Conference of the Parties to the Convention on Biological Diversity, known as the COP16, took place from 21 October to 1 November 2024 in Cali, Colombia. COP16 had a tough act to follow – at COP15, the long-anticipated Kunming-Montreal Global Biodiversity Framework (GBF) was adopted. Our key takeaways from COP15 and the implications of the GBF on corporates can be found here. In this post, we analyse some of the main outcomes of COP16 and their significance for corporates.

| Area (click to jump to section) | Implications for corporates |

| National Biodiversity Strategies and Action Plans (NBSAPs) | Corporates should be mindful of the NBSAPs of the countries in which they operate. These provide insight into potential changes in regulations and policy environments that might impact business operations. |

| Finance | There is an increased focus on the role the private sector can play in reaching finance goals under the GBF. Corporates may face expectations to increase contributions to biodiversity finance. |

| Subsidies | Environmentally harmful subsidies may face reforms, and recipients of such subsidies should prepare for shifts. |

| Digital sequence information | Whilst voluntary, companies might consider participation as an investment in maintaining their social license to operate and strengthening stakeholder trust. |

| Integrating biodiversity and climate change | Corporations might want to consider adapting strategies and transition plans to address and account for both climate and biodiversity issues. |

| Biodiversity credits | Companies may use biodiversity credits to offset biodiversity harms within their business. Companies relying on biodiversity credits as a key component of their sustainability strategy may face accusations of greenwashing, particularly if the credits are not tied to measurable, transparent outcomes. |

| Transition plans and disclosures | Even in the absence of any specific disclosure obligations relating to nature, the risks and opportunities arising from biodiversity loss are very likely to trigger legal obligations for companies and their directors under existing national company laws and corporate governance frameworks. |

| Lobbying | Companies should be cautious of misalignment between their communicated biodiversity commitments and lobbying positions, which may create reputational risks and lead to allegations of greenwashing. |

National Biodiversity Strategies and Action Plans

Prior to COP16, countries were required to submit national biodiversity strategies and action plans (NBSAPs) outlining how they would implement the GBF goals and targets. However, in October, an investigation found that 85% of countries were set to miss the deadline. COP16 resulted in the adoption of a new decision text on NBSAPs, which (amongst other things) urges those outstanding parties to revise or update their NBSAPs as soon as possible, and implement the NBSAP in accordance with national circumstances, priorities and capabilities.

What does this mean for corporates?

Companies operating within countries that have submitted NBSAPs or national targets should be astute to the plans and targets contained therein, which provide an insight into potential changes in regulations and policy environment which might impact business operations. For example, a number of the submitted NBSAPs include plans to establish frameworks for corporate biodiversity disclosures (discussed further below). Conversely, companies operating within countries that are yet to submit NBSAPs should note that the new decision text adopted at COP16 encourages Parties to enable the full and effective participation and engagement of the private sector; therefore, there might be an opportunity for companies to engage in this process.

Finance was a big focus of discussions at COP16. Target 19 of the GBF includes a goal to mobilise at least USD 200 billion a year for biodiversity conservation by 2030 from “all sources” (i.e., domestic, international, public and private). This includes a commitment for developed countries to commit at least USD 20 billion per year by 2025 and USD 30 billion per year by 2030, to fill a USD 700 billion ‘biodiversity finance gap’ (Goal D). Current finance commitments are falling short. One of the COP16 discussions focused on establishing a new global biodiversity fund, separate from the Global Biodiversity Framework Fund (GBFF). The GBFF – which was launched at COP15 and is hosted under the Global Environment Facility – aims to help countries achieve the GBF goals and targets, with a focus on strengthening national-level biodiversity management, planning, policy and governance. As with many COPs, discussions overran, and the eventual absence of delegates from developing countries broke the quorum, delaying a decision on the fund’s details.

What does this mean for corporates?

The private sector should be aware that Target 19 specifically calls out private finance as one of the sources from which the USD 200 billion is intended to be mobilised. There is an increased focus on the role that the private sector can play in reaching this goal. Corporates may face expectations to increase investments in biodiversity conservation through partnerships, direct funding, or the integration of nature-positive practices.

Target 18 of the GBF requires the identification of harmful biodiversity incentives (e.g., subsidies) by 2025, eliminating, phasing out, or reforming them, and progressively reducing such incentives by at least USD 500 billion annually by 2030. However, national implementation of Target 18 has been slow to date. Research has shown that in 2024, USD 2.6 trillion is being spent per year on environmentally harmful subsidies (EHS) – equivalent to 2.5% of global GDP.

What does this mean for corporates?

Change is likely afoot for sectors which are recipients of EHS. Such sectors include industrial agriculture (USD 650 billion in 2023) where subsidies are granted for petrochemical-based fertilisers that harm nature, and forestry (USD 175 billion in 2023) where subsidies flow to biomass companies turning forests to wood pellets to be burned – a process which emits more carbon emissions than coal. The opportunity to redirect harmful subsidies and scale up positive incentives for the conservation and sustainable use of biodiversity will likely be a continuing focus of future COPs.

Countries did manage to agree on a new benefit-sharing mechanism for genetic resources known as the “Cali fund”. Digital sequence information, or DSI, refers to the genetic information from plants and animals that are often sourced by companies headquartered in the Global North. There have long been calls for the establishment of a mechanism to equitably share the benefits from DSI with those where the information originated. The Cali fund is a step in this direction. The decision in relation to DSI specifies that companies that meet two of the following three criteria (averaged over the preceding three years) should contribute 1% of profits or 0.1% of revenue to the Cali fund: (1) total assets of USD 20 million; (2) sales of USD 50 million; or (3) profits of USD 5 million.

What does this mean for corporates?

Certain sectors will be impacted more than others, with the pharmaceutical, cosmetic and biotechnology and animal/plant breeding sectors specifically being called out. However, there are a number of limitations still within the text; in particular, the “should” terminology implies that contributing to the fund is still voluntary and that the payment rates are “indicative”, non-binding ones. Despite this, there are still compelling reasons for companies to comply. Companies might view participation as an investment in maintaining their social license to operate and strengthening stakeholder trust. Those who do contribute to the fund will need to consider how contributions will impact financial planning, forecasts and balance sheet implications.

Integrating biodiversity and climate change

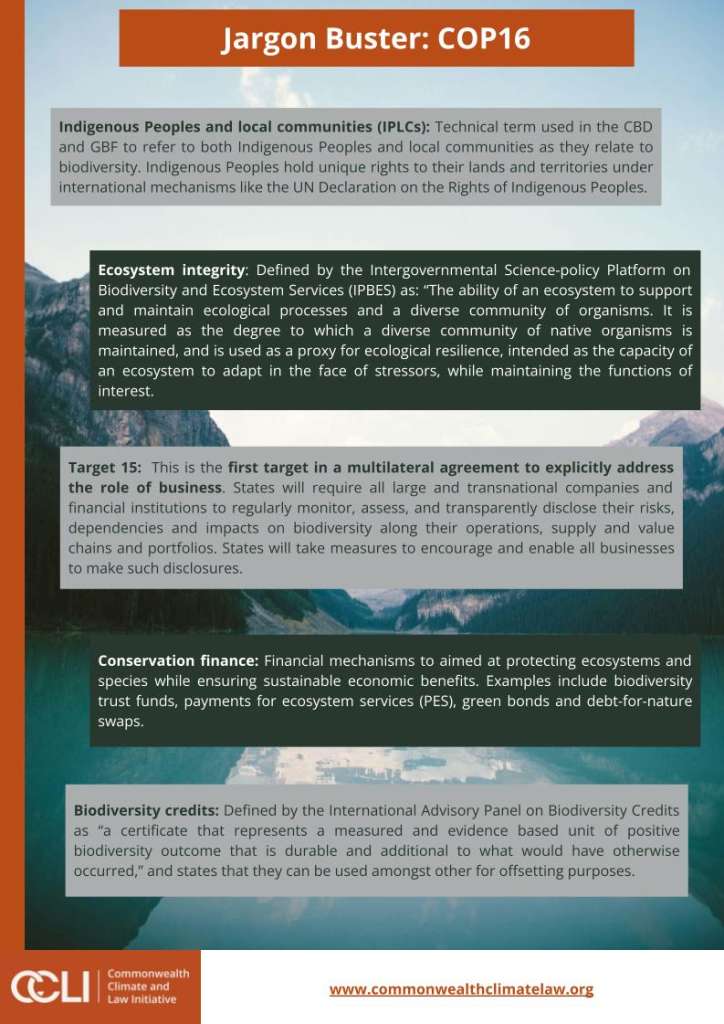

In light of Target 8 of the GBF and taking note of a Joint Statement on Climate, Nature and People issued at COP28 (the climate conference held in Dubai in 2025), a decision was adopted calling for enhanced policy coherence between climate change and biodiversity loss, recognising that these issues are intrinsically linked. The decision emphasises that biodiversity and ecosystem integrity play an important role in combating climate change and its impacts, and vice versa, that conserving and restoring biodiversity and ecosystems constitute actions towards minimising the impacts of climate change. The adopted decision urges countries to, amongst other things, identify and maximise potential synergies between biodiversity and climate actions and consider integrating nature-based solutions into their revised NBSAPs.

What does this mean for corporates?

While the decision does not directly mention the private sector, it will likely trigger further policy and legislative developments which will have a knock-on effect on the private sector. Corporations might want to consider adapting strategies and transition plans to address and account for both climate and biodiversity issues. Importantly, identifying synergies between climate and biodiversity actions could lead to business opportunities, such as cost savings, access to green finance, reduced nature and climate-related risks, improved resilience and long-term operational stability, and positioning the organisation as a sustainability leader.

Biodiversity credits are seen as an opportunity to raise biodiversity finance. However, they have been a hotly contested topic and were the subject of continued debate at COP16. The International Advisory Panel on Biodiversity Credits launched a framework for “high integrity” principles for biodiversity markets, which was supported by France and the UK. The framework recognises that as biodiversity is not fungible, a standardised biodiversity unit is not appropriate. It highlights the need for biodiversity credits to be local-to-local and like-for-like, and that Indigenous Peoples and local communities should be co-creators of projects and markets. However, the principles were criticised as being “extremely problematic”. Verra, a carbon-offset registry which itself has been the subject of scandal, also launched a framework for developing nature credits.

What does this mean for corporates?

Companies may use biodiversity credits to offset biodiversity harms within their business. This is especially the case with high-impact sectors (e.g., infrastructure, mining, agriculture). However, companies should be wise to the criticism that these markets have attracted. The absence of a universally accepted framework for biodiversity credits creates uncertainty for businesses looking to invest in or rely on these markets. Companies relying on biodiversity credits as a key component of their sustainability strategy may face accusations of greenwashing, particularly if the credits are not tied to measurable, transparent outcomes. Corporates might be interested in a new report by the World Economic Forum which provides guidance for the private sector on nature finance and biodiversity credits. The report notes that “businesses should be careful to avoid oversimplified, incorrect and misleading communication on biodiversity credits and markets”, and that alignment with the mitigation hierarchy is key with actions “that offer both financial and nature benefits by prioritizing avoidance, reduction and restoration, before offsetting”. Integrity in the market is crucial; corporates need a clear and material business case and clarity on how to link biodiversity credits to their business strategies and sustainability transition plans.

Transition plans and disclosures

Companies will be well aware of Target 15 of the GBF, which calls for countries to take measures to encourage and enable businesses and financial institutions to regularly monitor, assess, and transparently disclose their risks, dependencies and impacts on biodiversity. It is likely that when states enact disclosure regimes to implement Target 15, they will do so by reference to the Taskforce for Nature-Related Financial Disclosures’ (TNFD) final recommendations published in September 2023. In June 2024 the International Sustainability Standards Board (ISSB) published its 2024-2026 work plan, which includes a project to research disclosure about risks and opportunities associated with biodiversity, ecosystems, and ecosystem services. Relevantly, when undertaking this research, the ISSB will consider how to build on the TNFD recommendations. As such, it is likely that the global baseline for nature-related disclosures will closely follow the TNFD framework. A number of NBSAPs submitted by companies included references to the TNFD, including India and Japan.

Irrespective of mandatory disclosure requirements, investors are demanding nature-related disclosures. During COP16, an investor coalition of 27 of the world’s largest pension funds representing roughly USD2.5 trillion in assets under management urged governments to mandate corporate disclosures and nature-related transition plans, with disclosure expectations to include transparency on corporate lobbying and industry associations (more on this below). Business for Nature also released a statement from over 230 businesses and financial institutions, urging governments to follow the lead of others in requiring large businesses and financial institutions to assess and disclosure their nature-related risks, impacts and dependencies on nature. Other developments on the sidelines of COP16 included a consultation released by Glasgow Financial Alliance for Net Zero on ‘Nature in Net-zero Transition Plans’, which recognises the inextricable link between nature and climate, and a discussion paper published by the TNFD on draft guidance on nature transition planning for corporates and financial institutions.

What does this mean for corporates?

The Nature Action 100 Benchmark, which measures the initiative’s 100 companies’ progress toward its Investor Expectations for Companies, demonstrated that most of the initiative’s 100 companies are in the early stages of addressing nature-related impacts and dependencies. This is in line with the CDP, which reports that companies are still at the beginning of their journey to assess dependencies on biodiversity – in 2023, only 7% of companies and financial institutions disclosed that they assess their dependencies on biodiversity, while just over one-third plan to do so in the next two years.

The move towards mandatory nature-related disclosures is significant for corporates and their directors, especially if frameworks take influence from the TNFD, which follows a double materiality approach. Therefore, in addition to the recommended baseline of disclosing information that is material for users of general purpose financial reports (‘financial materiality’), the framework provides for additional disclosure of “topics that represent its most significant impacts on the economy, environment and people, including impacts on their human rights” (‘impact materiality’). Various proposed and enacted due diligence legislation around the world demonstrates that governments are responding to the elevated risk of biodiversity loss and climate change. Such legislation may have the effect of cascading information requests and increased transparency through value chains or ownership structures outside territories where the legislation is in force. For example, the under the EU’s Corporate Sustainability Reporting Directive (CSRD), which entered into force on 5 January 2023, biodiversity is integrated into reporting frameworks and guidelines that aim to assess and disclose the environmental impact of reporting entities. In February 2024, China introduced its mandatory sustainability reporting requirements, which also adopts a double materiality standard.

From a strategic management perspective, multinational companies will likely need to operate in line with the framework of the most ambitious regulator and therefore adopt a double materiality approach. Even if not operating in a country requiring nature-related disclosures, companies would be mindful to expand their reporting to include nature-related risks, opportunities, impacts and dependencies. This will likely require quantifying reliance on ecosystem services, obtaining data, and engaging with companies throughout the value chain. The TNFD’s LEAP guidance is a good place to start. Directors should also ensure that governance structures are in place to oversee nature-related risks and opportunities, integrating them into strategic planning and risk management processes. Nature-related issues need to be on the board agenda.

Even in the absence of any specific disclosure obligations relating to nature, the risks and opportunities arising from biodiversity loss are very likely to trigger legal obligations for companies and their directors under existing national company laws and corporate governance frameworks (see Biodiversity Risk: Legal Implications for Companies and their Directors). Directors’ duties to act with loyalty and care, requiring oversight of foreseeable and material risks and opportunities, are interpreted with reference to rapidly evolving market, social and regulatory context. Recent legal opinions published in the UK and Australia confirm that a failure on the part of a director to identify, manage and disclose material nature-related risks may lead to increased shareholder pressure, reputational consequences and potential liability.

Corporate and lobbying group attendance was high at COP16. In total, 1,261 business and industry delegates registered – more than double the number at COP15. Many of the industry groups present have a history of lobbying against regulations to protect nature, raising questions about the level of influence they had at the summit and its outcomes. This included Brazil’s Confederation of National Industry, which represents Brazilian agri-interests and has outlined its intentions to lobby for its member interests during COP16.

What does this mean for corporates?

Lobbying can be a legitimate method to influence government decisions and provide stakeholders the opportunity to participate in public decision-making processes. However, where lobbying activities are conducted without transparency and integrity, this can risk hindering progress and set a dangerous precedent whereby action to mitigate climate change and biodiversity loss is aligned with corporate interests rather than a just transition to net zero. Concerningly, research from Influence Map demonstrated that the world’s largest twenty companies lack transparency concerning their biodiversity-related advocacy. Companies should be cautious of misalignment between their communicated biodiversity commitments and lobbying positions, which can create reputation risks and allegations of greenwashing. See our article here on this subject. On the other hand, supporting nature-positive legislation can help create a stable regulatory environment that aligns with global sustainability trends and reduces uncertainty for businesses.

Summary

COP16 highlighted both the critical challenges and emerging opportunities in addressing biodiversity loss and integrating nature into global decision-making frameworks. The evolving landscape of biodiversity finance, corporate disclosures, and policy alignment underscores the growing expectations for businesses to play a proactive role in supporting nature-positive transitions. Attention now turns to Rome, where in February 2025 unfinished discussions will resume on important issues such as mobilising financial resources, and on strengthening transparency and implementation of the GBF.

This article does not intend to provide a comprehensive overview of all COP16 decisions and discussions.